Purpose

Small businesses often struggle to find available credit. Building on previous literature, this research analyzes what factors, including business credit scores, may explain credit outcomes (approvals or denials) for small businesses. It further asks what role business credit scores might play in the credit outcomes of women- and minority-owned small businesses.

Background

Credit Scores. Statistically derived and numerically presented, a “credit score” reflects an individual or entity’s likelihood of repaying a debt. Generally, a higher credit score correlates with a lower probability of default. The consumer credit market has utilized credit scores for decades, but small business credit scores emerged only during the 1990s. Large lenders adopted small business credit scoring in subsequent years.

Evidence indicates the emergence of business credit scoring may have increased credit availability to small businesses. A study of small business loan patterns indicates that banks using business credit scoring may feel able to make riskier loans at the margin and to increase their pool of available credit.

Still, while this study focuses on business credit scores, evidence indicates the credit market may make use of both consumer and business credit scores in determining small business credit outcomes. For example, a study using U.S. Small Business Administration data finds that community lenders may weigh consumer credit scores heavily in evaluating small firms, often to the exclusion of business credit scores. Such findings may prove relevant to policy determinations regarding the use and transparency of all types of credit scores.

Women- and Minority-Owned Small Businesses.

Pinpointing possible differences in credit access across race, ethnicity, and gender could prove important both to understanding varied credit outcomes and to policy determinations. For example, U.S. Census data indicate that minority-owned firms are smaller as measured by both sales revenues and employment, less profitable as measured by return on assets, and less likely to survive than their non- minority counterparts. In addition, women-owned firms tend to start with much less capital than their male counterparts, and Census data indicate women are also less likely to start or acquire firms with business loans from banks or financial institutions (5.5 percent of women owners versus 11.4 percent of male owners).

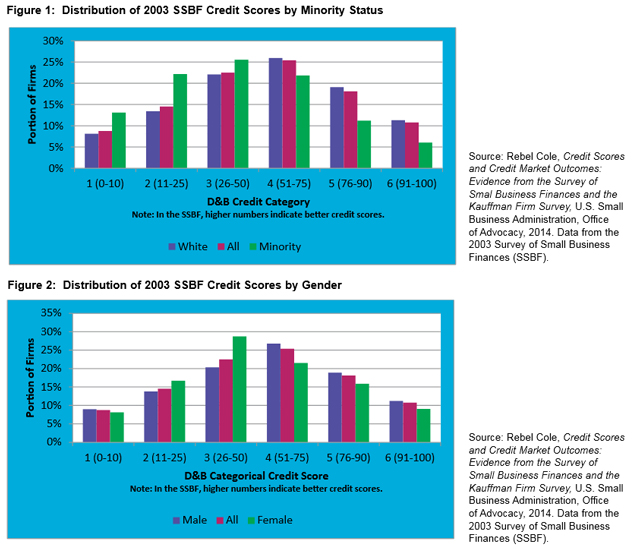

Several empirical studies have found evidence of disparate credit market outcomes for minority-owned small businesses. More specifically, several studies have found evidence of disproportionate loan denials to black-owned and Hispanic-owned firms, after controlling for other variables. This study confirms these findings and further asks whether business credit scores disproportionately affect access to credit for women-owned and minority-owned firms. Figures 1 and 2 illustrate business credit score distribution by race and gender.

Overall Findings

Regarding general access to credit, this study finds that small firms with lower credit scores are: (i) more likely to need additional credit because their credit needs have not already been met by past borrowings; (ii) more likely to be discouraged from applying for credit when they report a need for additional credit; and (iii) more likely to be denied credit when they need additional credit and apply for credit. Results also confirm prior findings that firm-lender relationships play a significant role in credit outcomes for small firms. Further, there is no evidence that credit scores reduce the importance of firm-lender relationships.

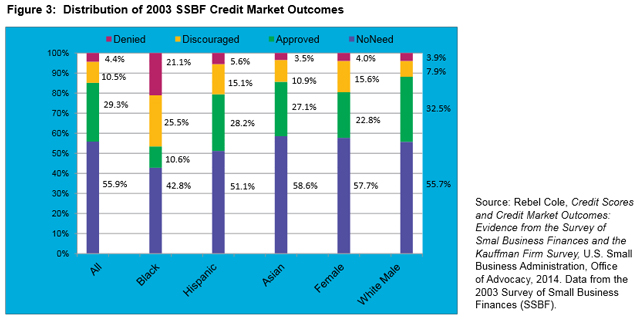

Empirical results also confirm prior findings that the credit market disproportionately denies credit to minority-owned firms when they need and apply for additional credit, after controlling for other variables. (See Figure 3 for a distribution of credit market outcomes by race, ethnicity and gender1). However, these results also indicate that credit scores do not disproportionately affect credit availability for either female-owned or minority-owned firms, relative to male-owned or non-minority-owned firms. In other words, the study did not find evidence that numerical credit score values were used disproportionately in credit determinations for minority-owned or women- owned firms.

Policy Recommendations

Evidence of disparate credit market outcomes for minority-owned businesses as well as the circumstances under which such possible discrimination occurs could prove relevant to policymakers. This study confirms prior findings of disparate credit market outcomes to minority-owned businesses in the form of loan denials but also further finds that institutions do not appear to use credit scores disproportionately in making credit determinations. This distinction in the results may help to narrow the field of policy variables that drive disparate credit outcomes to minority-owned small businesses.

For instance, while this study finds no evidence of disparate application of credit scores, it does not reach the question of what goes into credit score inputs and formulation. In addition, the use of consumer credit scores in small business evaluation may also have implications for transparency in credit score formulation. In a September 2012 report, the Consumer Financial Protection Bureau (CFPB) analyzed credit scores from 200,000 credit files from each of the three major U.S. credit-rating agencies and found that different models gave “meaningfully different results” for “a substantial minority” of consumers. In particular, the scores sold to consumers often differed from those sold to prospective lenders.

Further, this study reveals correlation between minority status and business credit scores and existing wealth. Such findings may inspire further research to explore disparate credit market outcomes for minority-owned small businesses in the context of wealth gaps.

Finally, the continued significance of relationship lending, as confirmed by this study, may indicate a need for further exploration of social capital issues among minority-owned and women-owned businesses. Recent studies have found that firm-lender relationships positively influence the decision to apply for a loan as well as the outcome. In particular, firms that report longer relationships with their prospective lender are less likely to be credit constrained.

Given these findings and their possible implications, further research and policy discussion may be merited.

Scope and Methodology

This study employs data from the Federal Reserve Board’s Surveys of Small Business Finances (SSBF) and from the Kauffman Foundation’s Kauffman Firm Survey (KFS) to evaluate whether credit scoring affects the availability of credit to women-owned- and minority-owned firms.

Using a three-step sequential logit model, the researcher poses the questions: who needs credit, who applies for credit, and who gets credit? Odds- ratio results indicate whether discernible relative differences in credit scoring impacts to women-owned and minority-owned firms occurred.

The research also uses descriptive statistics and observable data patterns to identify interesting correlations between gender, race and ethnicity, and industry relative to businesses credit scores.

This report was peer reviewed consistent with Advocacy’s data quality guidelines. More information on this process can be obtained by contacting the director of economic research at [email protected]

or (202) 205-6533.

By Rebel A. Cole, Krahenbuhl Global Consulting, Chicago, IL 60602. 78 pages. Under contract number SBAHQ-12-M-0168.

Additional Access to Capital Report

Disparities in Capital Access between Minority and Non-Minority Businesses: The Troubling Reality of Capital Limitations Faced by MBEs

» Executive Summary - Disparities in Capital Access between Minority and Non-Minority Businesses

» Download Report PDF 2.7MB

Connecting Small Manufacturers with the Capital Needed to Grow, Compete, and Succeed: Small Manufacturers Capital Access Inventory and Needs Assessment Report

» Download Report PDF 1.9 MB

Immigrant Entrepreneurs and Small Business Owners, and their Access to Financial Capital

» Research Summary

» Download Report PDF 257KB

1. Other variables include: firm characteristics, owner characteristics, and firm-lender relationships and are listed in detail in the results section of the study.

This document is a summary of the report identified above, developed under contract for the Small Business Administration, Office of Advocacy. As stated in the report, the final conclusions of the full report do not necessarily reflect the views of the Office of Advocacy. This summary may contain additional information, analysis, and policy recommendations from the Office of Advocacy.